The artificial services economy

The subject came up recently, about the effect of artificial intelligence (AI) on jobs and, presumably, the economy more broadly. The response was framed as a number of years away from that point of impact, and the ensuing retort likewise, albeit of much smaller numbers.

But technology does not advance in binary step functions (one day off, the next day on), it progresses; and its influence is not described in absolutes. What is more, the very definition of artificial intelligence is imprecise: it includes a future robotic form with human instinct and emotion, but also a present-day robot on wheels that picks up boxes. The voice on your device is powered by AI, but where should the line be drawn between it and a search result, or a shopping recommendation, a traffic instruction, or a robo-advisor portfolio? Is a digital network that tracks and records its own transactions not an intelligent solution? These and other mainstream examples precede the broader and deeper advances on the near-term horizon, determined by AI forms that beat Jeopardy contestants and Go players, and machines that teach themselves to create software, and cars that drive themselves.

With these progressions in mind, and a set of almost arbitrary definitions that in any case may be beside the point, the impact of it all on labor and the economy is similarly challenging to delineate concretely. Perhaps someone somewhere was let go because a software product was purchased, but possibly someone else was hired to manage the program. Maybe the ratio is not one-to-one, and maybe the two events were not in the same department, or the same company, or the same geography, or at the same time. And maybe the jobs do not pay similar wages.

The defining economic event of recent times, and the most monumental in the post-war era, is the transition to a newly digitized form of capitalism. The magnitude of this developing formation will likely be seen by future generations as similar in impact to the industrial and other major economic revolutions. Perhaps this current case is of even greater significance.

But the changes are happening now, we all see the changes, and so the questions are much less about where or when, than about how and what. We all think about these things, increasingly. What follows is a summary of some economic things I’m thinking about, in no particular order and without a real conclusion, except for a statement at the end that I believe is worthy of continuing reflection.

1. Mechanized knowledge

In Peter Drucker’s 1990s thesis, The Post-Capitalist Society, the author described a knowledge economy taking shape, dominated by knowledge work. This includes the professions of medicine, law, finance, engineering, science, but also all the services: administrative, retail, transportation, government and any others that involve an expertise of some kind, no matter how nuanced or straight-forward. Drucker’s vision has been well founded, but more to the point, we are now entering an era in which technology is increasingly capable of mechanizing much — often enough, most, and in some cases, all — of the expert knowledge and its work.

While differing in specifics according to the field, the collective ripple effects are noticeable throughout, particularly as consumers of knowledge services become accustomed to new technology applications and increasingly expect these and their continuing efficiencies to happen universally. As these applications in fact move to expand towards universality, and thus become ingrained in our culture, the pace of change and adoption is accelerating.

There is a turbulence that looms, with stirrings that have already started, because ours (as Drucker argued) is a knowledge economy — most vulnerable to disruptions in knowledge and its knowledge work and workers.

The described phenomenon — which seems increasingly fundamental and unlikely to reverse or cycle out — needs to be studied as a new economic subject, in the same way that productivity, imports and exports of material goods, inflation, labor statistics, etc., are studied to shape strategy and policy decisions. This new phenomenon impacts them all, and it may be that the grand measure itself, gross domestic product, will need to be revisited.

2. New industrial influencers

Besides the lower-level structural advances in data analytics and machine learning and other artificial intelligence, there are two noteworthy high-level phenomena that can be observed with growing clarity: (1) a convergence between previously disparate industries, as the language of software and data bits becomes a bridge between them; and (2) the outgrowth of digital networks with strong network effects that are increasingly dominant in economic competition.

- To substantiate the first point, note the growing overlap between offerings in commerce/finance/media in their modern manifestations (for banks, retailers, media companies), increasingly also showing parallels and combinations in transport/payments, and to varying degrees in many other information and process categories and between them. Also note the increasing integration of software and hardware that leads to similar and related convergences in the internet of things, and, most significantly perhaps (at least in its potential impact), automotive applications.

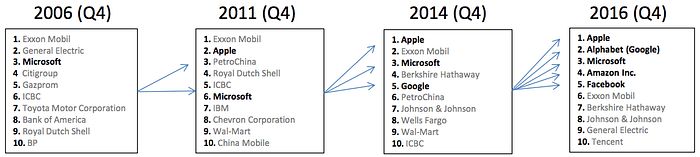

- In regard to the second point, for several months last summer/fall, the world’s top-5 most valuable public companies were, in order, Apple, Alphabet (Google), Microsoft, Amazon, and Facebook. (The latter two have since dropped a notch, due to the rise of Berkshire Hathaway, a substantial shareholder in Apple among others.) These companies not only exemplify the convergences of sector categories previously mentioned, but are multi-directional and multi-dimensional digital networks with strong network effects and network topologies that, as a result, are not likely to reverse course anytime soon.

The illustration presents a very different industrial scenario from what we saw even as recently as 5–10 years ago. A new analytic exercise may therefore prove insightful, on many levels, to quantitatively and qualitatively assess labor trends (as well as other economic drivers) within these leading organisms — and others that are growing quickly, or transforming, in their respective categories. Artificial intelligence is central to them all.

3. New competitive formations

The rapid evolution of multi-directional multi-dimensional networks with strong network effects, in combination with sector convergences as described, has perpetuated a “winner take most” competitive environment and a network ecosystem that is very different from earlier network manifestations. We are beginning to see these enormities emerge as disruptive forces shaping whole new areas (Uber, Airbnb, WeWork, Slack, to pick a selection of private names in addition to the previously referenced public counterparts), and we note related consolidations and combinations with similar effects in traditional segments (i.e., some of the leading names in telecom, finance, retail, and others).

This brings up several new considerations:

- While forming competitive barriers to strengthen their asset base, the network effects of the listed entities and others of similar size and stature is fueled by massive networked data troves. The “winner take most” environment thus runs parallel with a new phenomenon whereby — like banks that are “too big to fail” — now there are global data stores, possibly “too deep to fail,” or moving in that direction.

- If advisable at some point to break up, the integration of different network dimensions and the global reach (or potential) in today’s environment, will make that a very different exercise from, say, the regional fragmentation of Ma Bell at one time, in a different economy.

- The convergence of sector categories may also influence a different set of regulatory and anti-trust perspectives, especially with fading definitions of a company’s core business. (Is Apple really a hardware company? Is Amazon just a retailer? Are the car manufacturers going to be software/data applications before long? If so, will they compete with Amazon and Apple, too?)

In the longer term, the data-centric “winner take most” network phenomenon and its competitive dynamic could thus come to shape not only regulation and consumption of a company’s offerings, as noted, but its capital and labor needs for expansion or redirection. Much of that, in some form, will relate to data analytics (and artificial intelligence): that is everyone’s core product in a mechanized knowledge economy.

4. New aspects of consumption

Prevailing (low-cost) software operation and the efficiency enhancements created by digital data processing and its networked markets, have abbreviated the product commoditization cycle and led to a low-inflation or even deflationary product/service environment in many commercial categories. Exceptions exist, especially in the highly-regulated segments like healthcare, but deflation is anyway not a bad thing for the consumer to the extent net wages (i.e., after essentials) are stable or grow.

That assumption, however, has proven unreliable — in both top-line (gross revenue) and fixed costs (essential expenses) — for many individuals and businesses alike. The impetus to cut cost and seek out low-price items is therefore growing, on the supply and the demand side for similar reasons, leading to a circular loop whereby software applications are not just facilitators but fundamental to survival.

Based on the growing opportunity for such technology manifestations to conduct work in a knowledge/services economy, this is a pattern to watch with special attention.

5. Under-utilization and other imbalances

While software platforms do not require the same proportionate labor pool that comparably valued companies might in a non-technology manifestation, they also do not require the same level of capital allocation, because software is inexpensive to maintain and distribute.

With such bilateral capital and labor under-utilization as a backdrop, the leaders in a “winner take most” landscape have come to dominate their segments in steep power law statistical formations, wherein the long tail of the category may be almost completely marginalized. From a macroeconomic perspective, this suggests a disproportion.

It is possible that the steep power law phenomenon and its characteristic capital-labor underutilization is reflected in capital markets consolidations that have occurred. We see this in the growing dominance (and size) of the top funds and financial services organizations that intermediate fund flows.

These consolidations have brought with them a convergence of disciplines and activities: for instance, the venture capital category is almost entirely in pursuit of scalable software applications, while the more mature private equity funds are almost universally seeking scaled and recurring sales volume. Much falls between these polar masses, which may constitute missed economic potential, and missed employment opportunities.

In the public markets, the short-term hyper-efficiency that dominates is increasingly driven by data and the same software and AI mechanisms also driving the industrial mix that these markets track. The net effect has been a convergence (and commoditization) of viewpoints, noted by many as a diminishing incremental-return opportunity. As with private markets, there is a risk that such concentrations diminish long-term market efficiency, predicated on a multitude of viewpoints and diverse participation. It may be argued, in fact, that beyond the narrow confines of institutional capital markets, the health of the broader economy can itself be measured by the extent of individual participation as a linchpin, where capital flows deeply and broadly between optimal destinations.

Perhaps it already is. This is possible. But if so, it seems there is a corresponding outflow in a vastly uneven zero-sum distribution. There may, as a result, be a connection between the cited capital flows and observed labor under-participation (persistent for some time). Other variables also factor in, to be sure, but regardless of its relative extent and impact, the converging and networked software environment described in this article — which is itself what some refer to as “artificial intelligence” — will for the foreseeable future play a central part.

Related reading:

Ten questions for the new economist

Networks 3.0: defined by digital dimensions

Networks, products and their relativity